Debt First Aid Journey

When people fall into arrears, they often face challenging choices, from making significant lifestyle adjustments to pursuing formal debt solutions that may affect their future credit options. Our Debt First Aid Journey helps customers struggling to pay their bills and credit commitments to understand the options available to address their debt problems and take action.

Problem

According to the latest Financial Conduct Authority (FCA) Financial Lives survey, 7.4 million adults (14% of the UK adult population) feel heavily burdened by their bills and credit commitments, and 5.5 million (11%) have missed payments in the previous six months.

When people fall into arrears, they often face challenging choices, from making significant lifestyle adjustments to pursuing formal debt solutions that may affect their future credit options. The debt solution landscape is complex and difficult to navigate. Available options range from financial restructuring choices like debt consolidation loans to informal arrangements such as Debt Management Plans (DMPs), and formal solutions like bankruptcy.

Navigating these options requires extensive knowledge and experience, making it time-consuming to find the right solution. Addressing financial issues early is crucial for improving outcomes, as it helps prevent customers from falling further into debt and provides greater flexibility in choosing solutions to manage their debt.

Unfortunately, when people miss payments, many organisations provide only general guidance, such as money management advice or referrals to free debt advice services. This support often lacks personalisation, a clear call to action, and monitoring capabilities to ensure customers follow through on critical steps.

Opportunity

There is an opportunity to engage with customers earlier in their financial difficulties, incentivise them to act, and help them proactively address their debt problems. By taking early action, customers will have more options available, making it easier to resolve their debt issues.

For example, individuals can get temporary protection from their creditors through the Breathing Space scheme (Debt Respite Scheme in Scotland). While customers are still required to make their debt repayments during this period, the scheme provides temporary protection for up to 60 days, during which:

- Enforcement action cannot be taken against them.

- Creditors cannot contact them about debts included in the Breathing Space.

- Creditors cannot add interest or charges to their debt.

Additionally, customers can apply for a Debt Relief Order (DRO) or, in Scotland, a Minimal Asset Process (MAP). These are free-of-charge solutions designed to help low-income individuals address their debts. A DRO freezes debts for 12 months, and creditors stop taking action against them. At the end of the 12 months, the debts are written off.

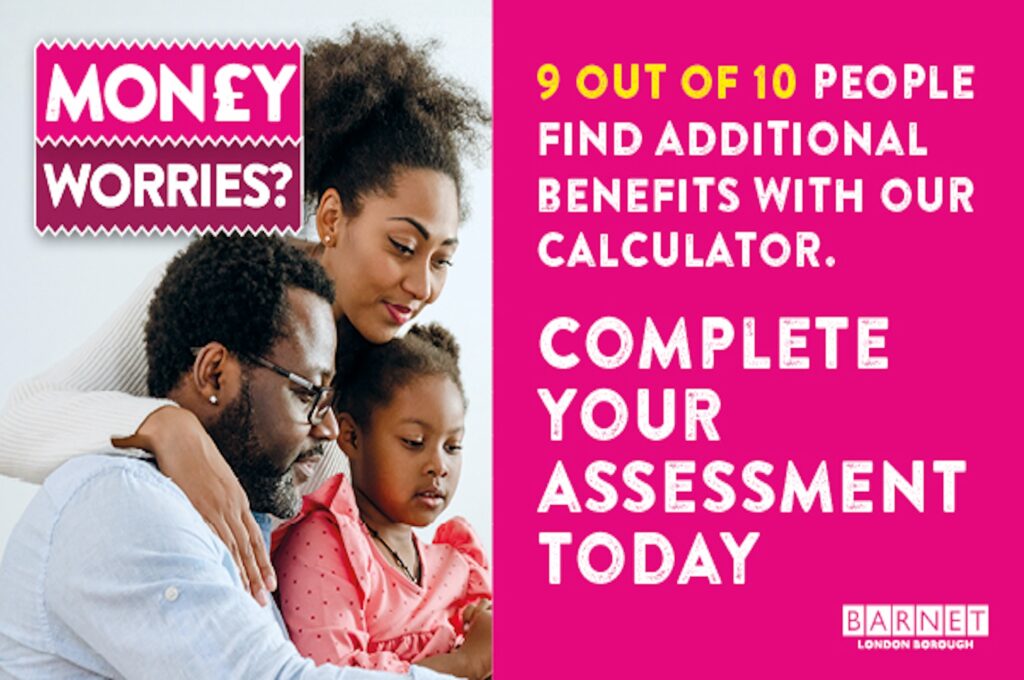

This is also an excellent opportunity to help customers access emergency funding and maximise their income. According to our data, two out of three customers are missing out on an average of £4,000 in benefits and discounts, which can significantly help improve their financial situation.

Solution

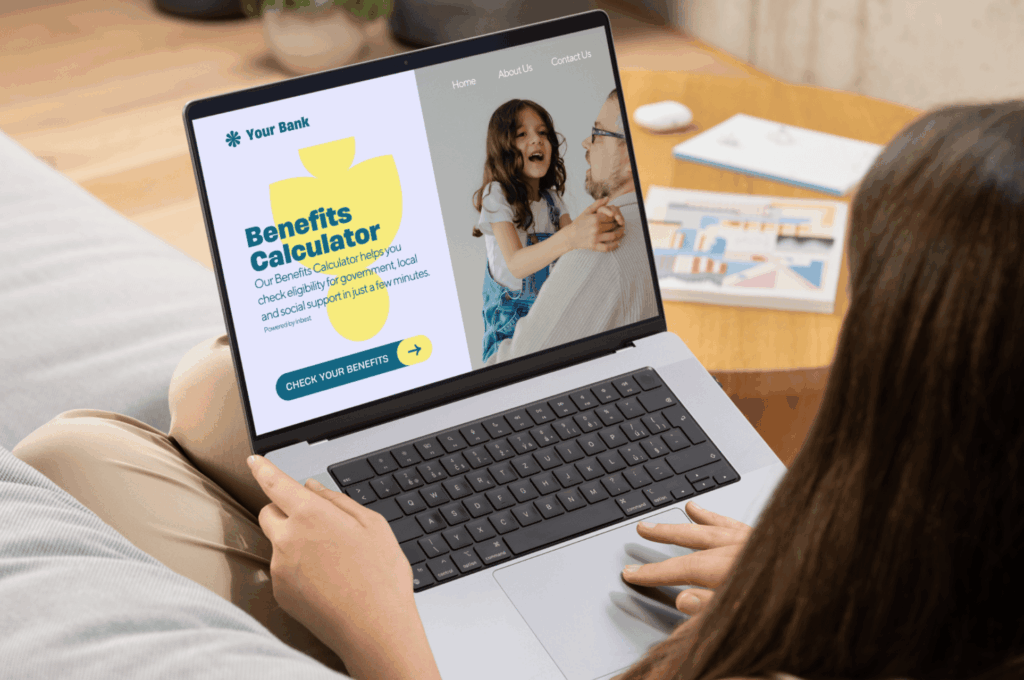

The Debt First Aid Journey is a one-stop support portal designed to help people struggling to meet their bills and credit commitments understand the first steps to address their debt issues. The portal presents customers with potential solutions based on their specific circumstances, financial situation, and available debt relief options.

By filtering potential solutions, the portal reduces the number of choices, prevents cognitive overload, and encourages customers to take action. However, it still presents enough options to give customers the freedom to focus on the actions they feel are most important. Customers will have a personalised dashboard to view their potential pathways, track their progress, and see the next steps they should take.

The solution leverages existing customer data to create customised journeys, presenting three types of solutions:

- Debt Solutions: We present potential options, including Breathing Space and Debt Relief Orders.

- Emergency Support: We offer information on emergency funding that customers can access, such as hardship grants, food banks, or support from their utility companies.

- Income Maximisation: We support customers maximise their income by helping them apply for national benefits such as Universal Credit or Child Benefit.

The Debt First Aid Journey includes an embedded CRM system that enables organisations to track customer actions, send personalised reminders, and offer tailored guidance. Additionally, the CRM helps regulated firms demonstrate compliance with FCA’s Consumer Duty.

FCA Consumer Duty

This solution helps FCA-regulated firms comply with the FCA Consumer Duty by ensuring that borrowers in financial difficulty are treated fairly. The Debt First Aid Tool ensures that customers in arrears understand their options and prioritise the solutions most favourable to them and in their best interests.

This tool also helps debt advice firms comply with the FCA Consumer Duty fair value assessments. For example, it ensures that customers are informed about the Breathing Space scheme and whether they are eligible for a free-of-charge Debt Relief Order before offering alternative debt solutions like Individual Voluntary Arrangements (IVAs).

Furthermore, this application supports consumer credit and mortgage providers in complying with the new FCA PS24/2 policy statement on strengthening protections for borrowers in financial difficulty. This policy aims to provide a more robust framework for firms to protect customers facing payment difficulties. It seeks to reduce and prevent harm to those who are in or at risk of payment difficulties by ensuring they are provided with appropriate support.

Book a Demo

Reach out to explore how our Debt First Aid Journey provides personalised support to those in financial difficulty, enhances customer engagement, and ensures compliance with regulatory requirements.