CASE STUDY: How Councils Can Use Administrative Data to Support the Delivery of the CRF.Learn more.

Menu

The FCA from Equality to Equity

The FCA is going to publish the “Guidance for firms on the fair treatment of vulnerable customers” in the next couple of weeks. In this new policy, the FCA highlights that protecting vulnerable consumers is a key priority for them and wants to ensure that these customers can experience outcomes that are as good as those for other consumers.

From Equality to Equity 👏

We find that the popular “equality and equity baseball picture” perfectly captures how the FCA is shifting their consumer protection focus from Equality to Equity. The principle of “fair treatment of customers” was a groundbreaking policy that triggered the outcomes-based regulatory approach across the world. While this regulation ensures that FS firms have good customer outcomes at the core of everything they do, it failed to address the special circumstances and needs of vulnerable customers. The new policy addresses this issue ensuring that FS firms provide custom tools and services that identify and address inequality.

Who is a vulnerable customer? 🆘

In short, most of us can be vulnerable as we can be affected by the following issues at some point in our lives:

Health: Health conditions or illnesses that affect our ability to carry out day-to-day tasks.

Life events: Major life events such as bereavement, job loss or relationship breakdown.

Resilience: Low ability to withstand emotional or financial shocks.

Capability: Low knowledge of financial matters or low confidence in managing money, or low capability in other relevant areas such as literacy or digital skills.

The first challenge firms face is to identify these drivers of vulnerability among their customers and measure their impact and severity. The objective is twofold, support customers who are at greater risks of harm, and act early to prevent the risk of harm growing…as the saying goes “an ounce of prevention is worth a pound of cure”.

How can we support vulnerable customers? 🧑🏿🤝🧑🏼

The FCA acknowledges that the standards firms should follow can vary widely due to the differences in services offered, firm size and customer base. However, firms should take the following steps to ensure that they are treating vulnerable customers fairly:

Understand the needs of vulnerable customers and explore how firms can support them.

Include controls to identify vulnerable customers and anticipate their needs.

Embed specific tools and services to support vulnerable customers across their customer journeys, including products & services distribution, customer services and communications.

Ensure that the staff has the skills, capability and tools to support vulnerable customers.

Monitor that the needs of vulnerable customers are being met, assess how they are resulting in good outcomes and mitigate the risk of harm to vulnerable consumers.

Potential solutions 🎯

While the FCA has defined the framework to better support vulnerable customers, it has taken a hand-offs approach in prescribing potential solutions. The FCA justifies this approach as prescribing minimum standards could result in the unintended consequence of “levelling down” the solutions implemented by firms. We go one step further, and we also believe that this approach will drive a wave of innovation as firms will face a clean-sheet design process to comply with this new policy.

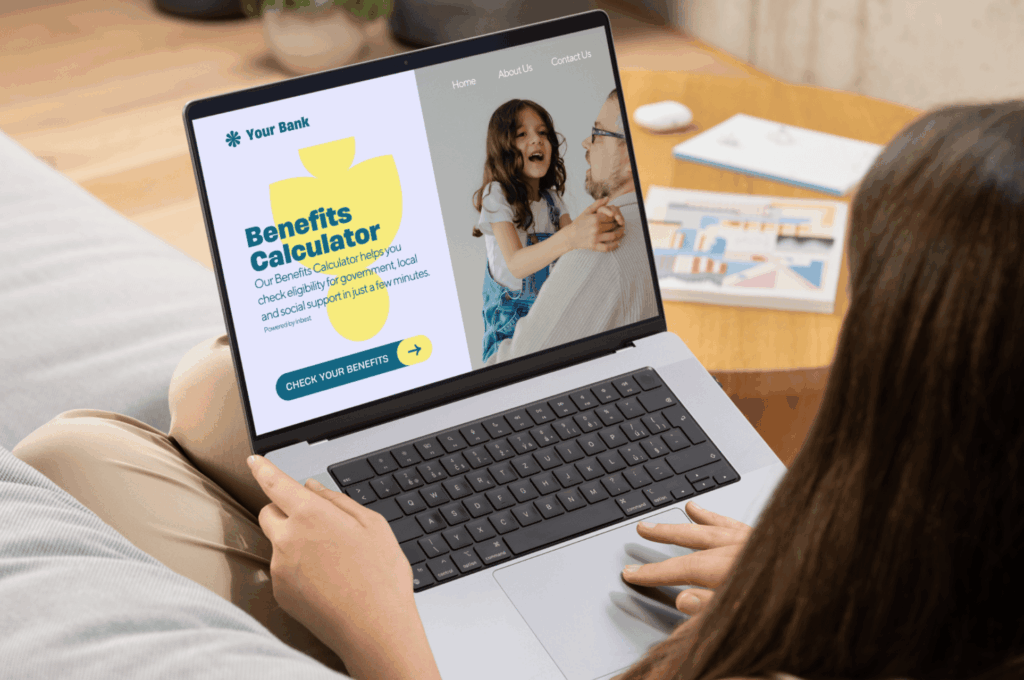

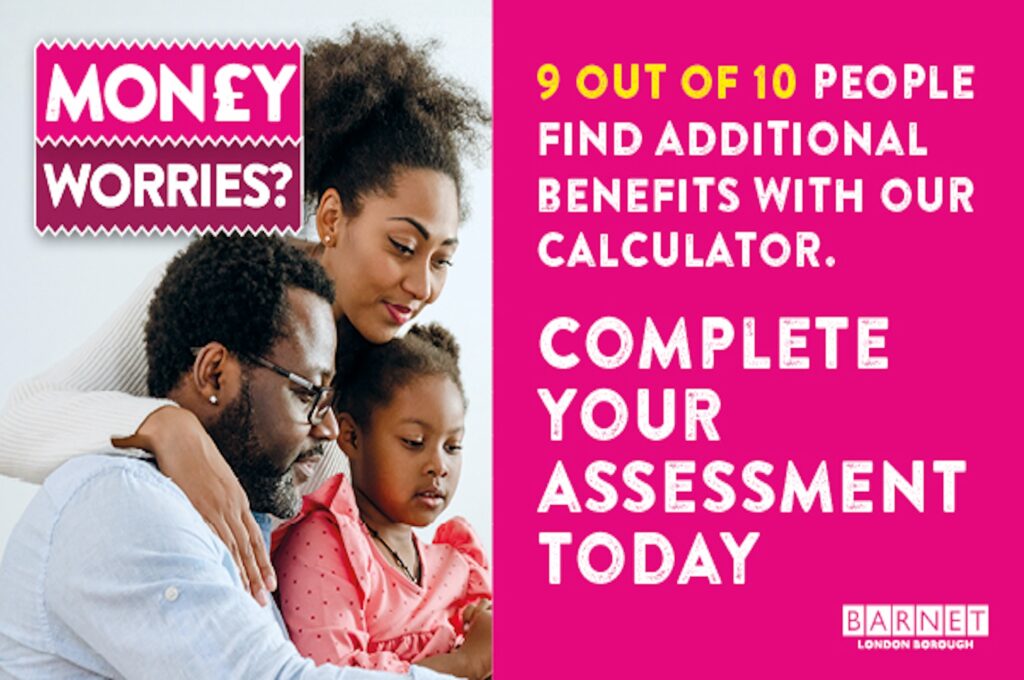

Inbest helps FS institutions to increase the engagement of vulnerable customers by making them aware of the benefits and grants available to them. FS institutions can embed Inbest benefits calculator across their customer journeys and demonstrate compliance with the FCA Guidance for firms on the fair treatment of vulnerable customers.

Contact us to view our platform in action and explore how we can help you to deliver your financial inclusion strategy.